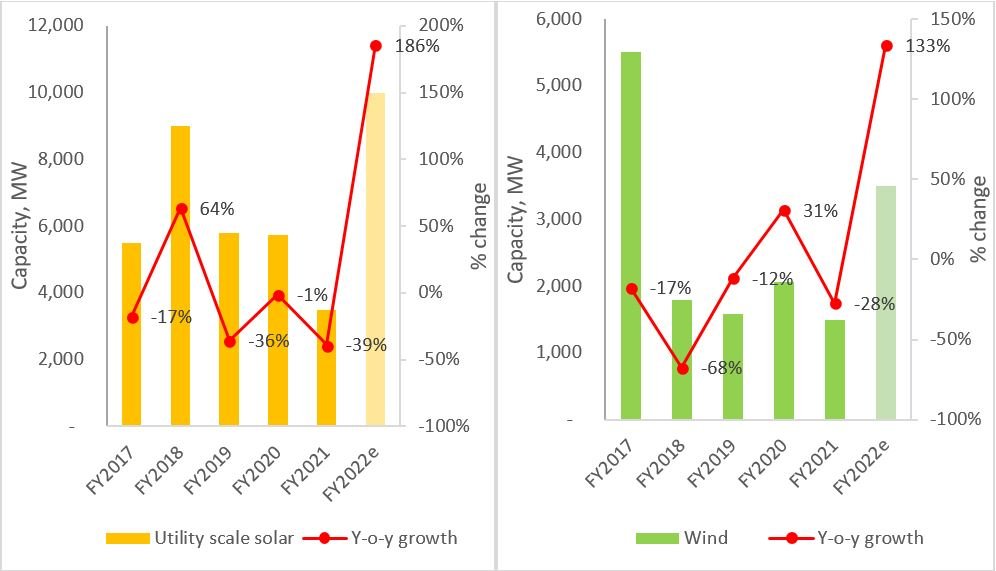

Utility-scale Solar installations declined 39% Y-O-Y in FY2021

In FY2021 (April 2020-Mar 2021), about 3.5 GW of new utility-scale solar capacity was added in India. Compared to previous year (FY2020), installations were about 39% lesser. Gujarat, Rajasthan, Tamil Nadu, Uttar Pradesh and Andhra Pradesh were the leading states with most of the large-scale solar installations during this period.

On the rooftop solar side, despite COVID-induced lockdown and restrictions, about 2 GW of new capacity was added in FY2021. Gujarat and Maharashtra together contributed nearly 50% of all rooftop solar installations in FY2021. Other states that added maximum rooftop solar capacity in FY2021 include Rajasthan, Tamil Nadu, Haryana and Uttar Pradesh. According to JMK Research estimates, the capacity addition in rooftop solar in FY2022 will be about 2.5-3 GW.

In the wind segment, in FY2021, about 1.5 GW of new wind capacity was added. This is about 28% lower than the previous year’s installation. Gujarat, Karnataka and Tamil Nadu contributed maximum wind capacity addition during this period.

Figure 1: Year-wise solar and wind installation trends in India

Source: MNRE, JMK Research

In the current fiscal year i.e. in FY2022, as per JMK Research estimates, about 10 GW of new utility-scale solar capacity and 3.5 GW of new wind capacity are expected to be installed. This is about 25% below that of our initial estimate which was made before the second wave of COVID-19 hit in India. Due to this, MNRE, in its recent notification dated 12 May, 2021, had stated that the renewable energy projects having their commissioning dates on or after 1 April, 2021, can claim extension owing to the second surge of the COVID-19 pandemic. MNRE also mentioned that, on receipt of an application for the time extension, the implementing agency would not initiate any coercive action on the project to recover penalty against delayed commissioning, until the extended time frame is decided upon.

Moreover, as there are lockdowns imposed across several states, there might be shortage of labour and delays in equipment supplies which might further lead to delay in commissioning of nearly 3-4 GW of solar and wind projects. Rooftop solar market too, might again face payment delay issues for OPEX projects as there is uncertainty looming over implementation of full or partial closure of manufacturing and business units. However, from a macro-perspective, industry growth in the future is expected to be highly positive as solar energy procurement still presents as a cost optimization channel. This has become more relevant amidst the pandemic where the C&I market’s price sensitiveness has become sharper.