Renewable Energy Tender Issuance In India not In Tandem with Government Targets

Report by IEEFA and JMK Research

Exceptionally successful reverse auctions drove the growth of solar and wind energy in India in the mid-2010s. The Solar Energy Corporation of India (SECI) is the key central government entity responsible for issuing new tenders, concluding auctions, and galvanising key Indian and global investor and corporate interests at scale. SECI accounts for almost half of all renewable energy tenders issued in India. However, India aims to achieve a 450 GW renewable energy target by 2030, requiring more tenders and accelerated efforts to mobilize investments and resources in this sector.

The total tenders issued for solar, wind and hybrid from 2010 to 2022 amounted to 161GW, with an allotted capacity of 114GW. Over the past few years, tendering (both issuance and allotment) of utility-scale projects (mainly solar and wind) has shown a downward trend and is not in tandem with government targets.

Variable Renewable Energy (VRE) tenders issued annually in India have fallen from 40GW in 2019 to about 28GW in 2022. Several contributing factors are leading to the recent slow uptake in renewable energy tender issuances, which challenges India to meet its renewable energy target of 450 GW by 2030.

First, there is a noticeable shift in the offtaker power demand profile. Despite VREs representing a very low share (11.5%) of the fiscal year (FY) 2022 electricity generation share nationally, distribution companies (DISCOMs) no longer prefer plain vanilla solar and wind projects. Instead, because of VRE’s inherent intermittency and seasonality, DISCOMs seek alternate clean energy solutions that offer more stable and firm power, such as wind-solar hybrid and renewable energy coupled with energy storage.

- To suit the need of DISCOMs, SECI is also accordingly transitioning to new age tenders with round the-clock (RTC) tenders, renewable energy tenders coupled with storage, and others. This has been a gradual process, and it has been a challenge to discover the optimum mix of technologies and tender conditions to arrive at suitable tariffs for both DISCOMs and developers. For firm renewable energy power, only pumped hydro storage technology, where tariffs range from Rs5-6/kilowatt-hour (kWh) (US$0.06-0.07/kWh), is the current viable option. Battery energy storage solutions (BESS) are still very costly, and the economics currently does not make financial sense without purchase power agreements (PPAs) supported by SECI.

- Some renewable energy-rich states like Karnataka and Andhra Pradesh have already achieved their renewable purchase obligation (RPO) targets. Hence, tender issuance from these states has slowed significantly in the past couple of years, despite the still-free interstate grid transmission access for VRE.

- A lack of participation from developers in some recent tenders is leading to undersubscription. Aggressive bidding and the failure of bidders to foresee a 30-40% rise in solar module prices have slowed developer participation due to the discovery of unviable prices in some tenders. Rising project costs due to the Approved List of Module Manufacturers (ALMM) and Basic Custom Duty (BCD) have also diminished the risk appetite of developers to bid aggressively on projects. The poor financial health of state DISCOMs leading to payment dues and the renegotiation of already executed contracts by certain states are other factors negatively affecting developer participation.

- Given that the tariffs discovered in auctions of new-age tenders are on the higher side, DISCOMs continue to rely on conventional thermal power. However, these newer wind and solar tender outcomes are still well below the realised wholesale price of electricity in India, given the imported fossil fuel hyperinflation of the last year.1

For India to reach its renewable energy target by 2030, it needs to add more than 30-35GW of new VRE capacity annually. However, the VRE tendering in India is still not in tandem with the targets. Various measures can address this:

- Future renewable energy tenders should consider the harmony of requirements between the energy generators (developers) and the offtakers (DISCOMs). It is imperative for the upcoming renewable energy tenders to have a balanced approach between driving down tariffs and maintaining healthy competition by reducing the financial stress as a result of excessively aggressive bidding.

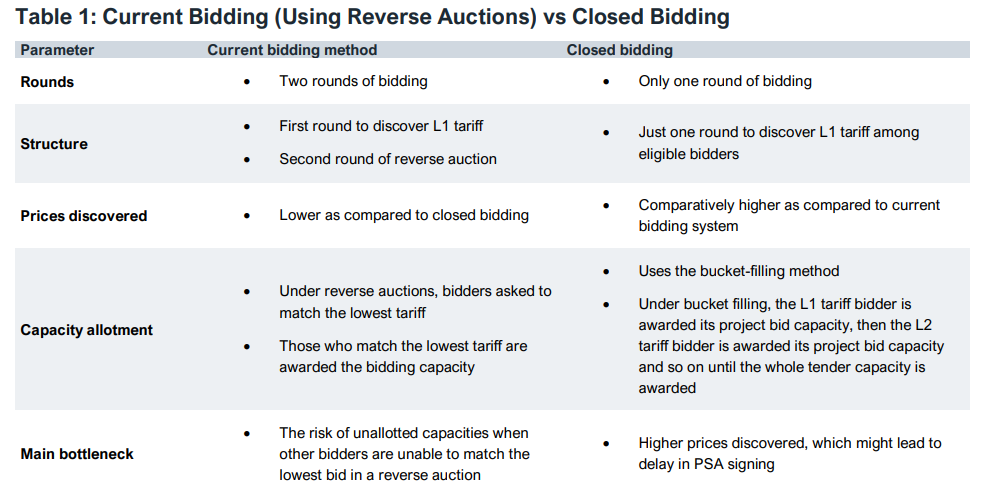

- The government is also planning to remove the reverse auctions in wind tenders to address the same issue. The bidding process will only consist of closed bidding to discover the L1 tariff. L1 tariff is the lowest quoted tariff among all the bidders in an auction. There will be no subsequent round of bidding to further drive down the prices.

Source: JMK Research

- To drive renewable energy sector growth, RPOs must be strictly enforced across all states with heavy penalties for failures to meet their renewable obligations.

- Payment security mechanisms should be strengthened to address developer fears of delayed payments, especially in state tenders.

With enhanced maturity of tendering authorities in the next couple of years to design inclusive and technologically balanced tenders, the more than 35GW target, although ambitious, seems attainable if SECI, NTPC and other state agencies can leverage the huge progress made to date. The global financial capacity and investment interest in India’s zero-emissions energy and grid infrastructure is a global success story that other nations are looking to emulate. Now is the time for India to leverage this enormous progress and double activity in domestic, deflationary, and zero-emissions electricity capacity expansions to diversify and strengthen the grid system while providing for the expanding energy needs to support India’s sustained, robust economic growth.

- Introduction

- Tender Issuance and Allotment Trends

- Factors Leading to the slow Uptake in Renewable Energy Tender Issuance

- What Needs to be Done?

- Conclusion

Enter the E-mail ID to download the report