Will ALMM Restriction Make A Dent On India’s Near-Term Progress?

On 13th January, 2022, the Ministry of New and Renewable Energy (MNRE) issued amendments to the ‘Approved List of Models and Manufacturers (ALMM) of Solar Modules (Requirements for Compulsory Registration) Order, 2019’. The new notification from the ministry points to the extension of ALMM scope to open access and net metering projects.

The objective of ALMM is to enhance domestic manufacturing and to have a quality benchmark for cells and modules. The ALMM order, 2019 provided for enlistment of models and manufacturers of solar PV cells and modules, in compliance with the BIS Standards, in ALMM list-I (Solar PV Modules) and ALMM list-II (Solar PV Cells). Further, as per the 2019 order, for list-I modules to be deployed in the concerned projects, the modules must mandatorily use the cells enlisted in list-II. However, only the list-I for modules has been published and regularly updated, whereas list-II for cells is yet to be released. List-I consists of 41 module manufacturers and a total enlisted capacity of 10.9 GW. This includes no foreign manufacturers or modules.

Therefore, only enlisted models and manufacturers of solar cells and modules complying with the BIS Standards in the ALMM list would be eligible for use in open access and net metering projects, in addition to government projects, government-assisted projects, projects under government schemes and programmes (for ex: Component A of PM-KUSUM scheme). The amendment is applicable for solar projects that apply for open access or net metering provision from 1st April, 2022.

The potential impacts of ALMM application on the solar sector are:

- Severe supply shortage: An estimated 18-20 GW of solar capacity is expected to be installed in India in 2022. And India relies on imported modules for about 70-80% of annual installed PV capacity. The cumulative operational capacity of domestic module manufacturing is just about 9-10 GW, a majority of which produce obsolete low-efficiency polycrystalline modules. Hence, solar project developers, with the demand for high-wattage (500 Wp+), high-efficiency (=/>20% CUF) modules on the rise, perceive huge supply paucity in the domestic PV manufacturing industry.

- Module price surge: Even considering the few top domestic PV manufacturers with the capacity to produce high-quality modules as desired by the developers (or investors), the challenge of higher module price becomes the major impediment. With paucity in eligible modules, the prices of domestic modules are anticipated to inflate substantially this year, which would lead to higher PPA rates.

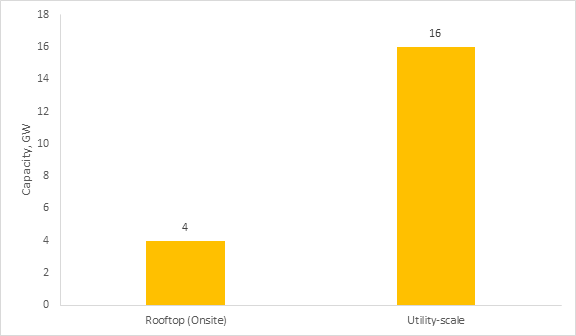

- Project delay: Currently, there are about 50 GW+ of capacity in-pipeline across rooftop and Open Access (OA) and utility-scale solar. Post the effective date of ALMM implementation, module procurement aspect for most of these projects would bear huge uncertainties, decelerating execution of under-development projects in the current year.

Figure 1: 2022 Capacity Addition Projections Across Rooftop and Utility-scale Solar

Source: JMK Research

ALMM, hitherto formulated, would primarily act as a major reinforcement to the existing non-tariff barriers against foreign module makers, while exacerbating the viability risks of potential new projects. In this scenario, extension of ALMM’s effective date for implementation is highly warranted, especially when annual solar installation of ~25 GW is required to meet the 280 GW solar target by 2030.