13.75 GW of new module and 6.9 GW of new cell production capacity likely to be added in India in next 18 months

More than 80% of India’s local demand for solar modules have been met through imports from other Asian countries such as China, Vietnam and Malaysia. In CY2020, India imported USD 1,527 million worth of solar cells and modules. The country’s ambitious target of additional 280 GW of solar power installation by 2030 along with its high dependence on solar imports warrants robust development of the domestic PV manufacturing industry.

At present, the cumulative solar cell and module manufacturing capacities of India are about 4 GW and 16 GW respectively. Additionally, the manufacturing capacity for upstream stages of polysilicon, ingot and wafer is absent in the current Indian landscape, on account of primarily, high production costs. Further, lack of scale and integration of PV manufacturing industry has been a critical barrier to the nation’s solarisation programme.

However, the Indian government, in a renewed effort to reduce import dependence and scale up domestic PV manufacturing capabilities, has introduced Basic Customs Duty (BCD) on imports and Production-linked Incentive (PLI) scheme for new manufacturing facilities. Effective from April-2022, the BCD on solar modules will be 40%, and on solar cells, it will be 25%. Aligned with India’s vision of becoming ‘Atmanirbhar’ and to catalyse India’s manufacturing capabilities, as part of PLI scheme, the government has committed Rs. 4,500 crores for ‘High-Efficiency Solar PV Modules’ which will be implemented by Ministry of New & Renewable Energy (MNRE). Under the PLI Scheme, 10 GW capacity of integrated solar PV manufacturing plants (from manufacturing of wafer-ingot to high-efficiency modules) will be set up by Q4 of 2022-23 with a direct investment of ~Rs. 14,000 crores.

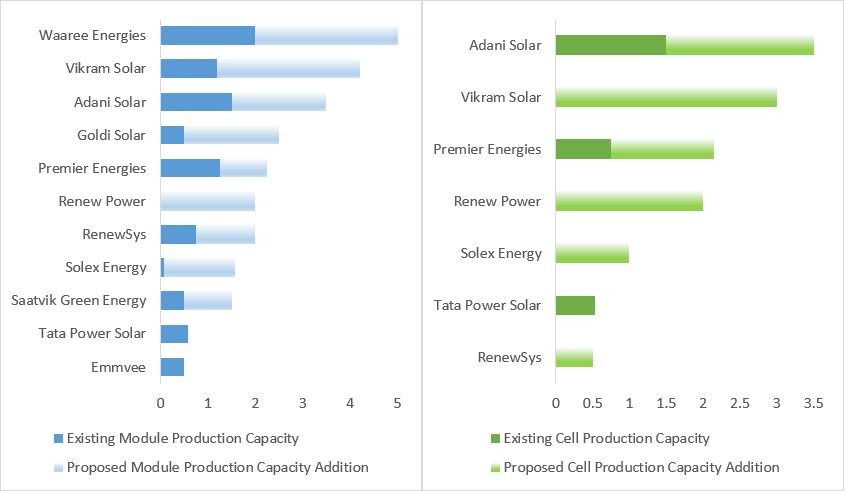

Several PV manufacturers, in this backdrop have committed to expand their existing manufacturing capabilities. Module manufacturers with 1 GW+ capacity (i.e. Waaree Energies, Adani Solar, Premier Energies and Vikram Solar) have proposed (in cumulative terms) module manufacturing capacity addition of 9 GW and cell manufacturing capacity addition of 6.4 GW. This also includes Vikram Solar’s plan to setup 3 GW solar PV manufacturing facility in Tamil Nadu in 4-5 years for manufacturing of solar modules, cells as well as wafers. As per media announcements, most of these players are expected to complete their respective capacity expansions (in total, module – 13.75 GW, cell – 6.9 GW) in the next 1-1.5 years.

In the current year so far, two key manufacturers accomplished a certain degree of expansion of their manufacturing capacities. In April 2021, Tata Power Solar expanded its manufacturing capacity of cell from 300 MW to 530 MW with mono-PERC and Module from 400 MW to 580 MW with mono-PERC, half-cut technology. In June 2021, Premier Energies has expanded its module manufacturing capacity from 500 MW to 1.25 GW and added 750 MW of cell manufacturing capacity.

Fig. 1: Key PV Manufacturers – Current Production Capacities & Proposed Capacity Additions (in GW)

Source: Company Websites, Industry News Articles, JMK Research

Note: Values mentioned in the table represent nameplate capacities.

Vikram Solar’s proposed 3 GW solar manufacturing facility would be involved in the manufacturing of solar modules, cells as well as wafers.

The Indian solar PV manufacturers are upgrading their capabilities to meet the evolving needs of the domestic and foreign demand for higher-efficiency modules. In terms of PV technology, mono-PERC (Passivated Emitter and Rear Cell) type is rapidly gaining prominence over multi-crystalline type. Industry experts believe that the domestic utility-scale solar market’s module preference would shift completely to mono-PERC by 2021-end.

Furthermore, wafer augmentation, i.e. the transition from M2 (156.75 mm2), M2.5 (158.75 mm2) to M6 (166 mm2), M10 (182 mm2), M12 (210 mm2) wafer formats, is facilitating the enhancement of module power output and efficiency. Soon, M6 wafer-based modules is expected to become mainstream in new domestic rooftop solar capacity additions. Also, domestic manufacturing capacity for bifacial modules is expanding as manufacturers foresee high growth potential in demand for these modules, especially from the residential rooftop market.

Additional module manufacturing capacity of 10 GW could lead to savings in foreign exchange (owing to import substitution) of around Rs. 17,500 crores per year[1].

Government should formulate plans now to support backward integration to set up cell, wafer and ingot manufacturing facilities as well as module manufacturing. State governments can intervene at these junctures by providing land, utilities, etc. at concessional rates and providing various regulatory approvals and permissions in a more timely and efficient manner. Further, innovation should be the core of all the government’s new plans. To achieve such local manufacturing strength, concerted efforts between the industry and government must be directed in buttressing potent policy and R&D initiatives.

[1] MNRE, Highlights – Budget 2021-22 – Provisions for Renewable Energy (RE) Sector