Total enlisted module capacity under latest ALMM list crosses 18 GW and 66 manufacturers

The government introduced “Approved List of Models and Manufacturers” (ALMM) in 2019-20 to benchmark Indian manufactured solar cells and modules as well as support development of domestic manufacturing industry. All government utility scale, net metering and open access projects were mandated to use only ALMM enlisted modules from April 2022. However, for net metering or open access projects, the deadline was later extended to October 2022.

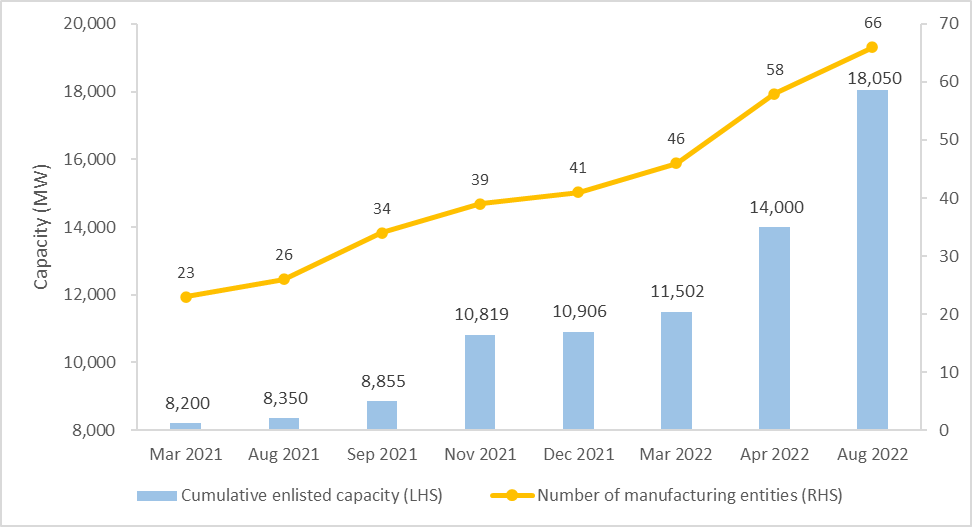

The first ALMM list containing 23 manufacturers and a total enlisted capacity of 8,200 MW was issued in March 2021. Since then, there have been further 7 revisions to the list in a span of 18 months. As compared to the first list issued just 18 months back, the enlistment capacity has risen to 18,050 MW (2.2X increase). During the same period, number of enlisted manufacturers has almost tripled to 66.

Figure 1: ALMM enlistment trend

Source: JMK Research, MNRE

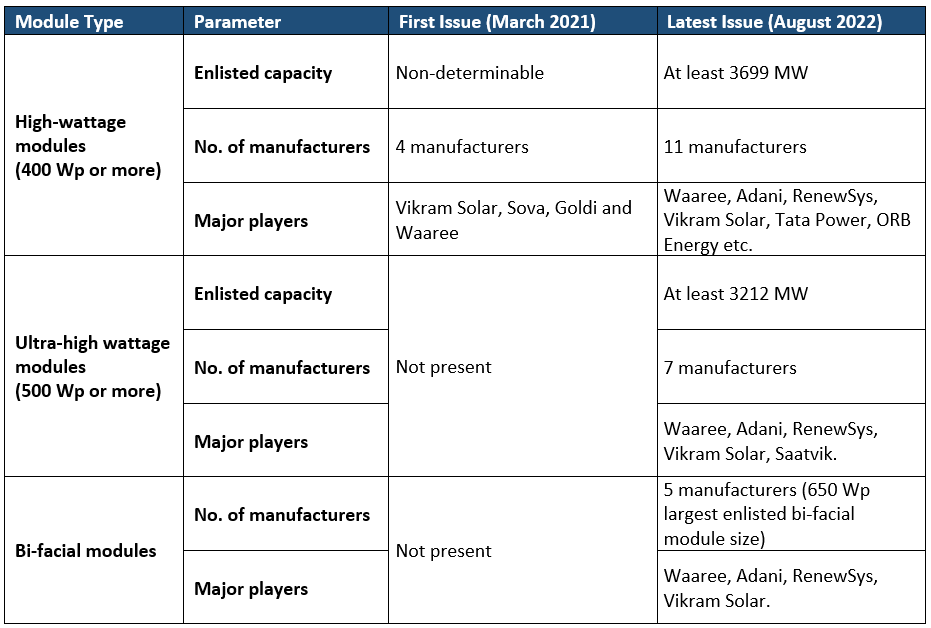

While solar manufacturers have largely been supportive of ALMM, the developers have frequently cited concerns. The main concern has been paucity in enlisted capacity of high-wattage high-efficiency modules that are usually preferred in C&I installations. The latest ALMM list (August 2022) addresses these concerns and provide positive outlook to whole domestic PV manufacturing industry.

Table 1: ALMM comparison in terms of high-wattage modules enlistment (March 2021 vs August 2022)

Source: JMK Research, MNRE

According to the latest ALMM list, there are 11 domestic manufacturers which can supply high-wattage modules (i.e., 400 Wp or more). Out of these 11 manufacturers, 7 manufacturers can supply modules in the ultra-high wattage range as well (500 Wp or more). Additionally, there are two manufacturers offering 600Wp+ modules also.

RenewSys have specified that 487 MW of their installed production capacity will be for high-wattage modules. Also, Waaree and Adani specified that 2,650 MW and 562 MW of their installed production capacity will be for ultra-high wattage modules. The list also contains 5 manufacturers with bi-facial modules production capacity. The largest module enlisted is 650 Wp by Waaree. This module comes in both Mono PERC and bi-facial formats.

Table 2: Domestic players manufacturing high-wattage, ultra-high wattage and bi-facial solar modules (as per ALMM list issued in August 2022)

Source: JMK research, MNRE

Availability of these high wattage modules in ALMM is very important to quell fears of developers who were concerned about compromised generation due to lack of availability of these modules. Current high wattage module enlisted capacity (~6-7 GW) is not enough to cater to overall Indian annual solar demand (viz. ~20 GW). However, the fast-paced growth of this capacity provides all stakeholders with confidence.

Observing the table above, the evolution and growth of Indian PV manufacturing capability in past 18 months is evident. Indian manufacturers are employing larger wafer sizes (such as M10, M12) to produce high-wattage and ultra-high wattage modules. M10 wafer size is generally used to manufacture ultra-high wattage (500 Wp+) modules while M12 is employed in manufacturing 580Wp+ modules. GW-scale manufacturing facilities have increased substantially. It is expected that by 2025, India will have 51 GW of annual module production capacity[1]. Majority of this upcoming capacity will be high-wattage high-efficiency modules. A major credit for this growth can also be accredited to positive outlook created towards PV manufacturing by government through schemes such as Production Linked Incentive (PLI).

India is at a critical point in terms of solar energy adoption and advancement. If the focus of nurturing the sector is purely upon project development, domestic manufacturers become laggards. Also, if the entire focus shifts to manufacturing indigenously, the developers most likely bear the major costs in terms of importing materials. All stakeholders must now decide on a balanced and sustainable PV development road map for the country. It will require a fine balance between the manufacture and consumption of solar PV equipment domestically. For e.g., to support developers, until domestic manufacturing is significantly increased, the government can look at short-term inclusion of Chinese manufacturers in ALMM. Also, to support upstream domestic PV manufacturing, government should concurrently come up with ALMM list for solar cells, as mandated in original ALMM order.

[1] JMK Research, Photovoltaic Manufacturing Outlook in India, February 2022