Rooftop solar financing options for Prospective customers

This is the fourth and final blog of our four-part blog series to assess and analyze the different routes via which C&I rooftop solar players are raising much-needed investments to further scale this sector and accelerate growth. So far, we have dived into Equity investments, Mergers, and Acquisitions and understood various debt instruments via which the majority of investments come from, and have identified the key players. In this blog, we will look into the various loan options available for rooftop solar projects.

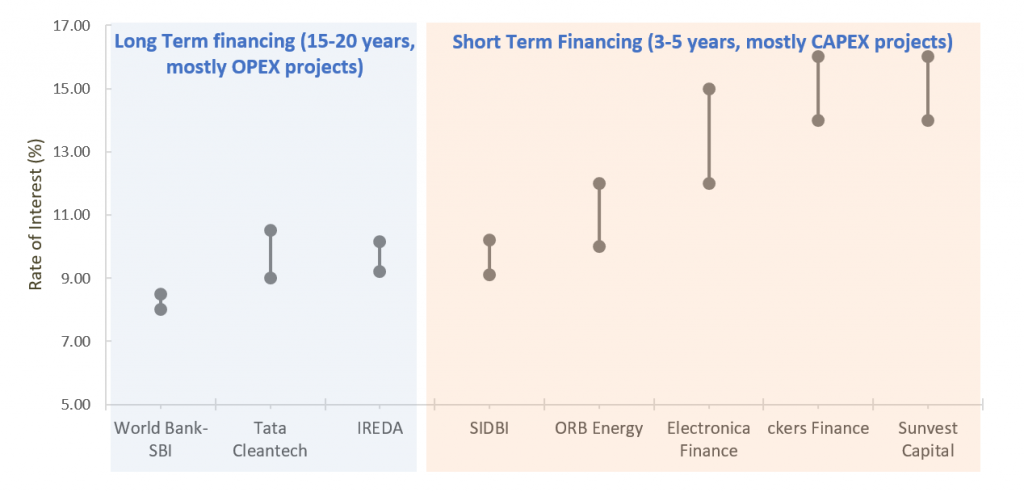

Based on the loan tenures, the loan options available can be categorized in terms of long-term loans and short-term loans. As depicted in figure 1, long-term loans tend to have lower interest rates vis-a-vis short-term loans. Long-term loans, however, can in most cases be availed by only those customers who opt for OPEX installations and have a proven financial track record to minimize default risks.

Fig 1: Key Lenders in Rooftop Solar Sector in India

Source: JMK Research

Long Term Financing

These are typically availed by corporate players with BBB+ credit ratings and above. The loan tenor is on the longer side (in the range of 10-25 years). Financing under this category is usually availed under concessional credit lines made available by development banks and multi-lateral agencies.

World Bank-SBI line

The World Bank-State Bank of India (SBI) fund for rooftop solar is a US$625m fund, with an additional US$23m allotted for technical assistance and first-loss coverage. The program started in May 2016 and the deadline is November 2021, however it is likely to get extended given the amount of funds remaining to be disbursed. As of December 2020, World Bank has disbursed US$463m to SBI, out of which US$228m (49%) have been disbursed by SBI for a cumulative project portfolio of 451 MW. While there is no distinction as such between OPEX and CAPEX, minimum project sizes are 100kW for CAPEX models and 1 MW total portfolio for RESCOs. To give thrust to smaller size projects, a customized loan product for projects up to 1 MW capacity is designed under this fund scheme. Although initial progress has been slow in terms of disbursal of loan from World Bank SBI concessional credit line, however, it is likely to pick up pace in next few years now.

Tata Cleantech- GCF line

Tata Cleantech is another major lender in this space, which has availed funds from Green Climate Fund (GCF). Tata Cleantech is a joint venture between Tata Capital Limited and International Finance Corporation (IFC), World Bank Group. These loans are offered at an interest rate of 9-10%, and the loan tenure depends on the length of the PPA term and the credit worthiness of the customer. Majority of the projects financed under this fund are based on the OPEX model.

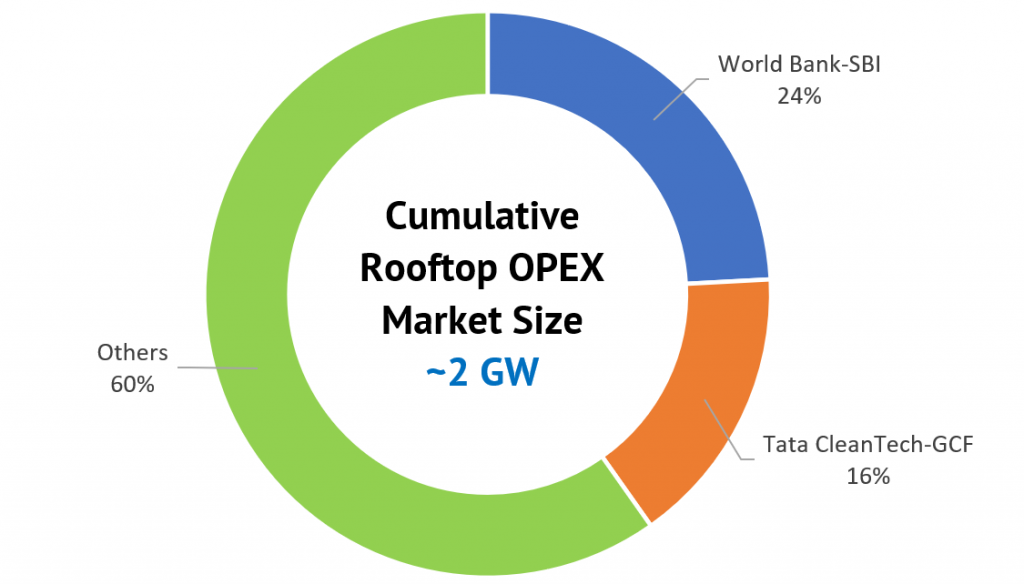

The World Bank-SBI line and Tata Cleantech-GCF together account for 40% of the OPEX market as illustrated below.

Fig 2: Rooftop Solar OPEX share Funded under different debt mechanisms, as of July 31, 2021

Source: JMK Research

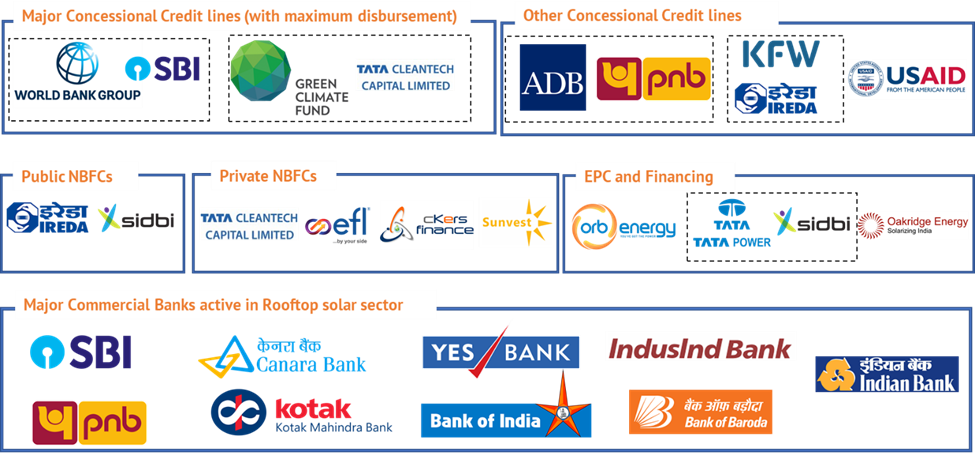

Apart from these, banks such as Canara Bank, Bank of Baroda, Bank of India, and Indian Bank, are some of the lenders who provide non-concessional credit schemes.

Fig 3: Active institutions/lenders in the rooftop solar financing market

Source: IEEFA, JMK Research

Short Term Financing

Short term financing options are usually for a tenor of up to 5-7 years, and are mostly availed either by MSMEs or by corporates who could not avail loans from the abovementioned route. Major lenders in this space are SIDBI and Orb Energy.

Orb Energy

Orb Energy is an interesting business case, as it is one the few players in this segment to build a successful business. Headquartered in Bengaluru, Karnataka, Orb has sold more than 160,000 solar systems, with cumulative installations of more than 110 MW of rooftop solar systems, of which more than 30 MW has used Orb’s in-house financing. One of the main reasons for its success is because the company does both, EPC as well as project financing, enabling to get higher margins as compared to other players in the market.

Small Industries Development Bank of India (SIDBI)

The SIDBI loan for rooftop solar (STAR Scheme) is a loan specifically targeting MSMEs to help them optimize their costs. The loan is offered for a period of 5 years with interest rates between 9.1% to 10.2%, covering upto 100% of the project costs with a minimum of Rs. 10 lakh up to Rs. 10 lakh. The project size is capped between 25kW and 500kW, and the power output should be lower than the current consumption from the grid.

Bridge Financing

Bridge loan financing is a type of gap financing arrangement under which the borrower gets access to short term loans for meeting their short-term liquidity requirements. These loans have higher interest rates of about 12-14%. Loans via this route are generally availed by consumers in the early stages of construction. Lenders providing these loans do so on the assumption that the customer will apply for project refinancing once the rooftop solar asset generates energy, which reduces its risk. If not done, it increases the NPA risks for lenders. Other major lenders in this space are Electronica Finance Limited, Sunvest Capital, Metafin cleantech finance, cKers Finance and Oakridge Finance are some relevant NBFCs in this segment.

While the rooftop solar installations in India have been growing over time, the growth has been not as stellar as in the utility solar segment. However, with increasing accessibility to affordable finance, rooftop solar installations are expected to grow further in the C&I Segment. This growth is also expected to extend in other segments such as MSMEs and the residential segment, which remains relatively untapped.