Registered EV sales drop 20% Y-o-Y in FY2021

The sales trend of Electric Vehicles in India during the fiscal year 2020-21 (FY21) is a rather distinguished case. Across this period, the EV market pursued the trade from one extreme reality to another. The monthly (or even quarterly) sales which began as abysmally low (owing to covid-19 induced disruption) transformed into the highest-ever registered figures by fiscal-end. The registered EV sales during Q1 of FY2021 shrunk 73% Y-o-Y to 8,387 units whereas the Q4-FY2021 sales rose by 33% Y-o-Y to reach 61,401 units.

Fig. 1: FY2021 Quarterly Sales Trend – Registered EVs

Source: Vahan Dashboard, JMK Research

Note: Sales figures represent EVs registered across 1,286 RTOs in 33 states/ UTs.

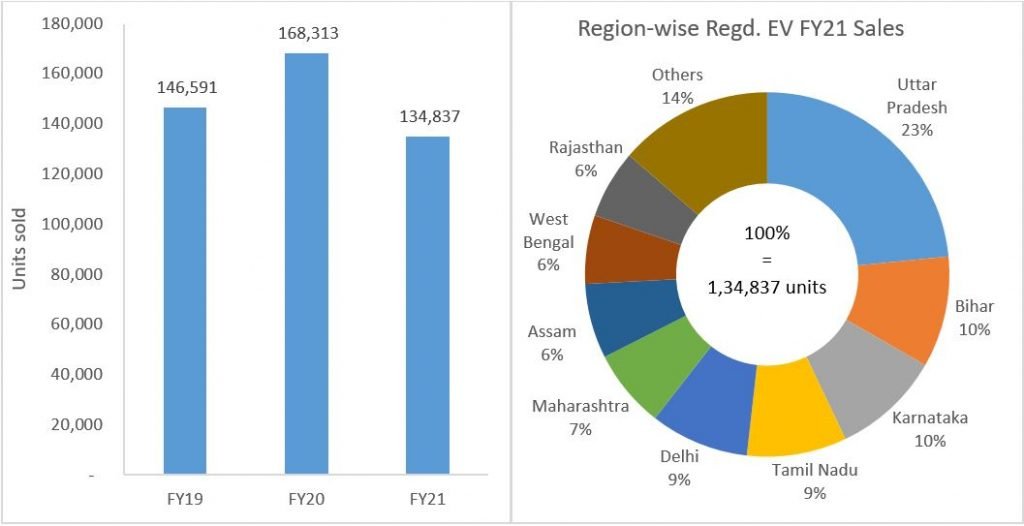

Despite an average 94% Q-o-Q growth from Q1 to Q4 of FY2021, the sales during the corresponding fiscal year plummeted 20% below that of FY2020, failing even to cross the FY19 sales level. The highest FY sales record of 1,68,313 units of FY2020 remains to be beaten. With regard to the (state/UT) region-wise sales, Uttar Pradesh has a clear lead with 23% share of total registered EV sales in India, followed by Bihar and Karnataka with 10% share each.

Fig. 2: FY Sales Trend – Registered EVs

Source: Vahan Dashboard, JMK Research

Note: Sales figures represent EVs registered across 1,286 RTOs in 33 states/ UTs.

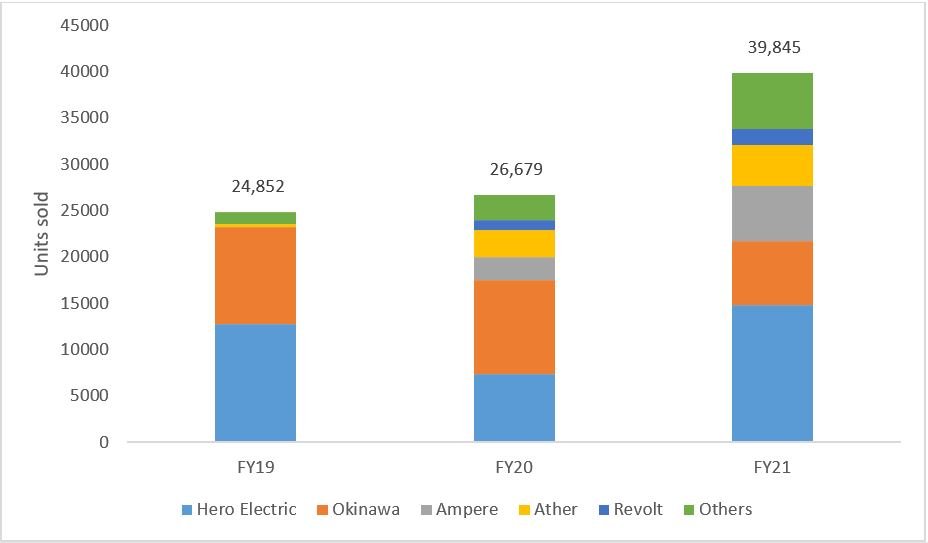

In FY21, the High-Speed Electric 2-Wheeler (HS-E2W) segment advanced significantly, registering 49% Y-o-Y growth to reach 39,845 unit sales. Among the HS-E2W OEMs (Original Equipment Manufacturers), Hero Electric sold the maximum number of units, attaining ~37% share of the market, which was followed by Okinawa and Ampere with ~18% and ~15% market shares respectively.

Fig. 3: High Speed (Registered) Electric Two-Wheeler Sales Trend

Source: Vahan Dashboard, JMK Research

Note: Sales figure are for only high range E2W models with speed higher than 25kmph. Sales figure represent E2Ws registered across 1,286 RTOs in 33 states/ UTs.

Assumption: Sales of top players- Hero Electric, Okinawa, Ampere, Ather, and Revolt together constitute 95%, 90% and 85% share of the total HS E2W market in FY19, FY20 and FY21 respectively.

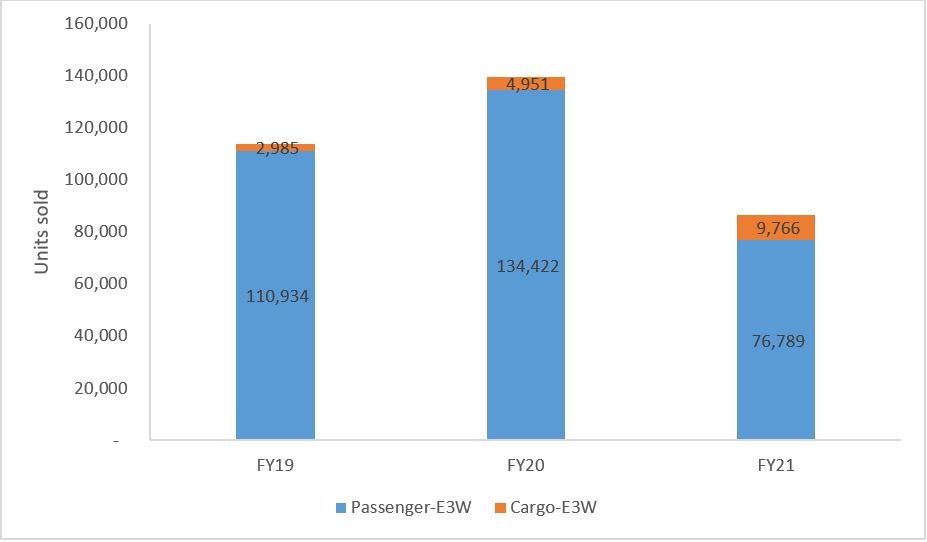

The (registered) Electric 3-Wheeler (E3W) sales in FY21 declined by 38% Y-o-Y to reach 86,555 units. This was mainly driven by the steep fall (-43%) in the sales of the passenger type E3Ws. However, the sales of Cargo-E3Ws rose by 97% over the same period, taking the share of Cargo-E3W to 11% of the total registered E3W sales.

Fig. 4: Registered Electric Three-Wheeler Sales Trend

Source: Vahan Dashboard, JMK Research

Note: Sales figures represent E3Ws registered across 1,286 RTOs in 33 states/ UTs.

The accelerated Q-o-Q growth can be expected to continue well into the ongoing fiscal year FY2022 on account of increasing consumer awareness, introduction of a sizeable number of new models, and technological advancements along the EV value chain which will lead to realization of greater value for money. In addition to this, effective central and state-level policy interventions in terms of fiscal and non-fiscal incentives (in addition to the ones that are already in place) are also necessary to nurture and sustain the relevant ecosystem.