More than 23 GW of RE assets acquired in India So Far

With the demand for renewable energy growth in India , more and more companies are vying to get hold of a considerable share of the Indian RE market. Some of these companies are either entering the Indian RE market or expanding their existing portfolios via inorganic routes such as by acquiring commissioned and/or under-development RE assets. This is also a preferred route whereby developers are able to avoid various greenfield RE projects related issues such as land acquisition hurdles, delays in obtaining relevant regulatory approvals, etc.

Through acquisition deals, these companies (or buyers) can takeover fully- or partly-implemented RE asset(s). On the other side of the deal, the investees (or the sellers) cash in on their RE asset(s) either to raise money for developing new projects or to exit the RE market.

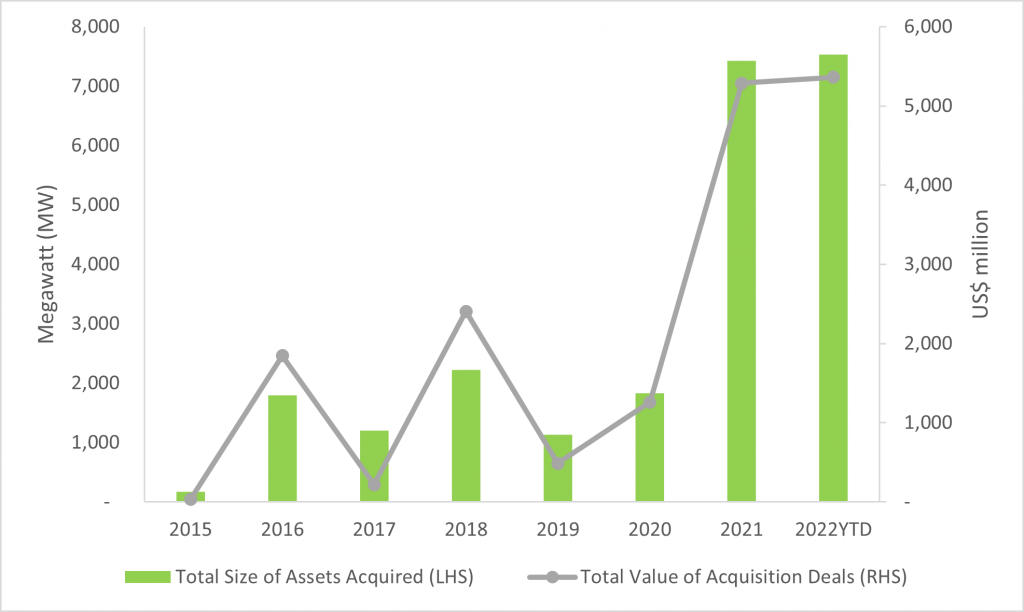

More than 23GW of RE generation assets (including plain vanilla solar, wind and hydro, and wind solar hybrid projects) in India changed hands via acquisition-type deals. From 2016 to 2020, total annual volume of RE asset acquisition hovered around 1.5GW. However, in 2021 and 2022YTD, the total annual volumes are 7GW+ each.

Figure 1: Annual Acquisition Trend of Indian Renewable Power Generation Assets

Source: News Articles, JMK Research

Note:

1) Only those acquisition deals whose deal value and acquired assets size are publicly disclosed have been taken into account in the above figure.

2) The RE portfolio depicted above includes operational and under-development assets.

Some of the major acquisition deals indicating renewable energy growth in India over the past few years include:

Table 1: Some of the Major RE-linked Acquisition Deals in the Indian Context

|

Date |

Asset Seller/ Investee |

Asset Buyer/ Investor |

Deal value (US$ Mn) |

Portfolio Acquired (MW) |

Asset Technology |

|

13-11-2022 |

Vector Green |

Sembcorp Industries |

474 |

583 |

Solar+Wind |

|

02-06-2022 |

Undisclosed |

Renew Power |

388 |

528 |

Solar+Wind |

|

20-05-2022 |

Mytrah Energy |

JSW Energy |

2,000 |

1,753 |

Solar+Wind |

|

29-04-2022 |

Sprng Energy |

Shell |

1,550 |

2,900 |

Solar+Wind |

|

04-10-2021 |

SB Energy |

Adani Green Energy |

3,500 |

4,954 |

Solar+Wind |

|

11-08-2021 |

L&T |

Renew Power |

384 |

359 |

Solar+Hydro |

|

22-06-2021 |

Fortum |

Actis |

335 |

500 |

Solar |

|

01-03-2021 |

Engie (India) |

Edelweiss Infrastructure Yield Plus |

550 |

813 |

Solar |

|

01-04-2019 |

Amplus |

Petronas |

391 |

500 |

Solar |

|

10-10-2018 |

Orange Renewables |

Greenko |

850 |

907 |

Solar+Wind |

|

02-04-2018 |

Ostro Energy |

Renew Power |

1,550 |

1,100 |

Solar+Wind |

|

07-11-2016 |

SunEdison |

Greenko |

392 |

587 |

Solar+Wind |

|

13-06-2016 |

Welspun Renewables Energy |

Tata Power Renewable Energy |

1,400 |

1,140 |

Solar+Wind |

Source: News Articles, JMK Research

Note: The RE portfolio depicted above includes operational and under-development assets.

The largest RE generating company (Genco) acquisition deal in 2022 year-to-date (YTD):

- In terms of RE portfolio acquired, was the Shell-Sprng Energy deal in August 2022. The deal was valued at US$1.55 billion and it envisages acquisition of 2.9GW of solar and wind assets of Sprng Energy by the oil and gas giant Shell.

- In terms of deal value, the JSW-Mytrah Energy deal was the largest RE Genco buyout deal (valued at US$2 billion), second only to the largest-ever deal in the Indian context – the US$3.5 billion Adani-SB Energy deal (2021). With this deal, JSW would have complete ownership of 1.75GW of RE assets of Mytrah Energy.

SB Energy (backed by Softbank), Skypower are few major international developers that have exited the Indian RE market. Pivoting to the international players relevant in the inorganic route, Shell, Sembcorp Industries, Actis, ThomasLloyd, Petronas Group are some of the companies that signed-up for brownfield investments in the Indian RE landscape. Together these players acquired 8.3GW+ of RE assets.

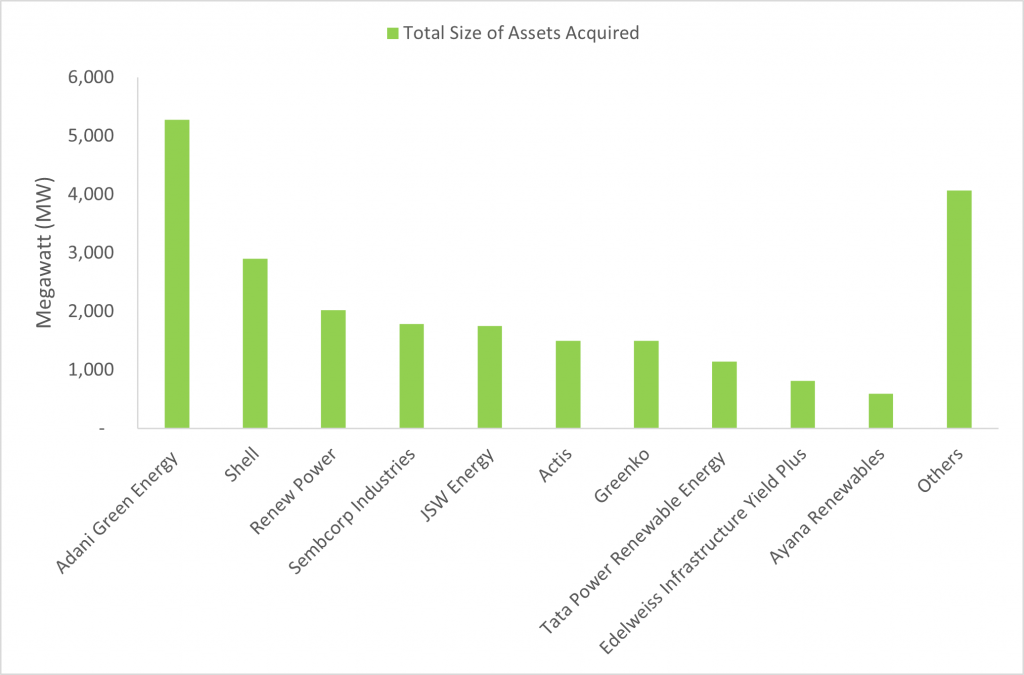

Further, of all the relevant domestic and international players, Adani Green Energy purchased the maximum volume of RE assets via acquisition (5.2GW+) thus far, which is followed by Shell (2.9GW) and Renew Power (2GW+). Players such as Adani, Renew Power have been aggressive along both organic and inorganic routes. Whereas, players such as Shell, JSW, Augment Infrastructure, O2 Power stepped onto the inorganic route just in the recent past.

Figure 2: Player-wise Status of RE Portfolio acquired till date (as of Nov 30, 2022)

Source: News Articles, JMK Research

Note:

1) Only those acquisition deals whose acquired assets data is publicly disclosed have been taken into account in the above figure.

2) The RE portfolio depicted above includes operational and under-development assets.

In the coming years, RE asset acquisitions is expected to increase further, indicating renewable energy growth in India. This will be owing to a large number of companies with diverse backgrounds strengthening their focus on ‘greening’ their energy portfolios. Many small as well as large companies with attractive PPAs on their existing assets may also look at selling them to build their future pipeline capacity. This will aid in meeting the national target of achieving 50% share of RE in the overall installed capacity by 2030.