Latest 6.4 GW Andhra Pradesh solar auction saw uptrend in tariffs

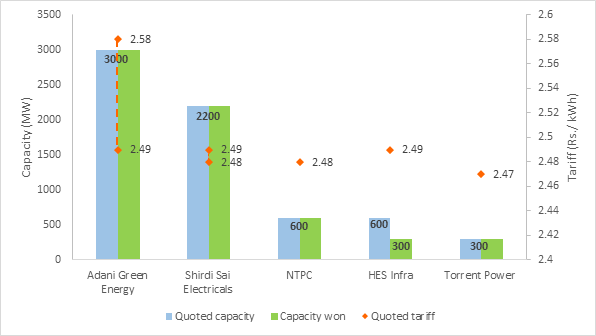

In an apparent recalibration in solar market dynamics, India’s largest solar auction of 6.4 GW by Andhra Pradesh Green Energy Corporation Limited’s (APGECL) registered lowest price (L1) of Rs. 2.47 per kWh by Torrent Power for 300 MW capacity. The L1 tariff is significantly higher than the record-low tariffs of Rs. 1.99 – 2 per unit, discovered in the previous auctions of GUVNL 500 MW Solar (Phase XI) auction and SECI 1,070 MW Solar (Tranche-III) auctions respectively.

The other winners in the APGECL 6.4 GW Solar Ultra Mega Solar auction include NTPC who quoted a tariff of Rs. 2.48 per unit for 600 MW. Adani Green Energy ltd.(AGEL) won 3 GW of solar projects across 5 different locations (600 MW each), quoting bid prices in the range of Rs 2.49-2.58 per unit, whereas, Shirdi Sai Electricals placed bid prices in the range of Rs. 2.48-2.49 for a total bid quantity of 2200 MW capacity, winning 4 solar park projects. Finally, HES Infra, although having bid for 600 MW at Rs. 2.49 per unit, was allocated 300 MW capacity only.

These 5 players submitted a combined 14.9 GW of bids, oversubscribing the tender by 8.5 GW. Out of these 5 players, HES Infra, a civil contractor firm, and Shirdi Sai Electricals, a transformer manufacturer, are the new entrants that have participated for the first time.

The objective behind issuance of this tender is to distribute free solar power to Andhra Pradesh’s farms for 30 years. The designated solar project locations are situated in Anantapur, Kadapa, Kurnool and Prakasam districts.

The projects will be awarded only after the outcome of a writ petition filed in the High court of Andhra Pradesh by Tata Power Renewable Energy alleging that the terms of RfS and PPA are in contradiction to the Electricity Act, 2003. As part of the conditions laid in the tender document, the payment-related disputes for the plants will be taken up by the state government mechanisms instead of SERC or CERC.

The discovered tariffs in this auction brought a “revision” in solar tariff trends in the Indian market, denoting that the earlier unprecedented low tariff of Rs. 1.99–2 per unit might be purely on a situational basis. Following are the possible reasons:

- Higher risks associated with the earlier PPA renegotiation issues with the AP government.

- Low solar irradiation level compared to Rajasthan.

- Less competition because of no participation from International developers or PE-funded companies in the auction. Partly also because of lesser time for bid submission because of which many players were not able to conduct detailed site assessment.

Fig.1: APGECL 6.4 GW Solar Auction result

Source: JMK Research