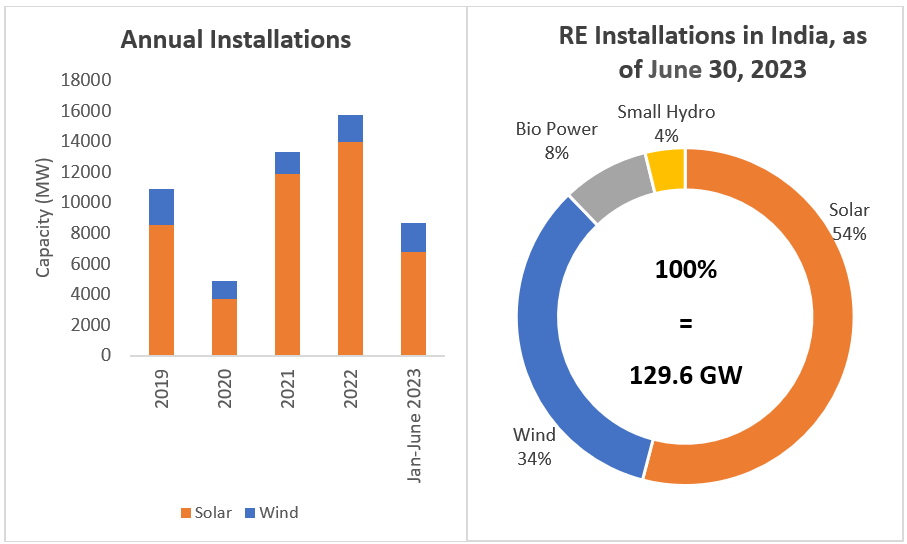

H1 2023 Recap: Solar Installations fell by 19%, wind rises by 166%

From January 2023 till June 2023, about 6,794 MW solar capacity and 1,878 MW wind capacity was added in India. Solar capacity addition is about 19% lower compared to the same period in the previous year. However, within the same period, wind sector has shown remarkable improvement with around 166% higher installations.

In terms of cumulative installations till June 2023, according to the Ministry of New and Renewable Energy (MNRE), India’s renewable energy (RE) installed capacity reached 129.6 GW. Solar energy contributes approximately 54% share of the total RE segment, an increase of 3 percentage points (from 51%) in last 12 months.

Figure 1: RE installation trends in India

Source: CEA, JMK Research

Note: Solar capacity includes utility-scale solar, rooftop solar and off-grid/distributed solar capacity.

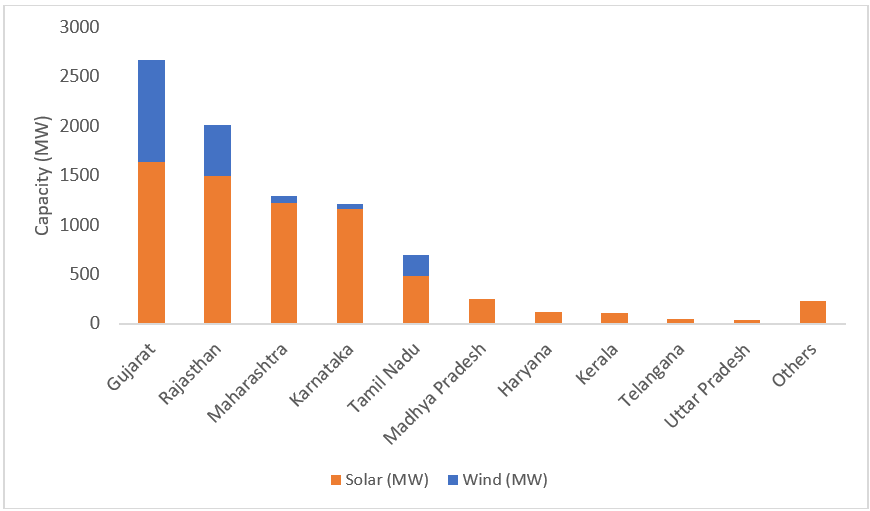

In terms of state-wise solar installations, in the first half of 2023, Gujarat leads with 1.6 GW capacity. Owing to its attractive Wind Solar Hybrid policy, Gujarat also leads in the wind installations with 1.039 GW installed during H1 2023. Significant contribution in wind capacity in Gujarat in last 6 months is also from private PPA/ open access market.

Figure 2: State-wise Capacity Addition in India (During January to June 2023 Period)

Source: MNRE, JMK Research

The installed capacity in wind in H1 2023 has already surpassed overall calendar year 2022 installation figures. Removal of reverse auctions and declaration of annual 50 GW tendering trajectory by the government will further reinvigorate the wind sector.

Within solar, rooftop segment has also shown significant uptake in installations. In H1 2023, around 2,294 MW of rooftop solar capacity is added, which is higher than the entire installations in this segment in CY2022.

In H2 2023, additional 1.5 GW of wind is likely to be added while in solar, additional 7-8 GW is expected. Significant fall in solar module prices over last few months as well as relaxation in ALMM implementation until FY2024 will be the key drivers to augment solar capacity addition in second half of the year.

Solar sector contribution to India’s national target of 500 GW non-fossil fuel capacity by 2030 is proposedly around 280 GW. Thus, a yearly augmentation of about 30 GW of solar capacity would be required.

Attaining this ambitious target would require concurrent development of all segments (utility scale, open access, rooftop, etc.) of solar industry. Considering the laggardness of rooftop solar market so far, it is highly imperative to have a greater focus on, and put more concerted efforts towards, the growth of this segment. Additionally, to mitigate supply chain risks, it is critical to enhance domestic solar manufacturing capabilities.