5.3 GW of Floating Solar Projects under various stages of development in India

Last week, Uttar Pradesh Cabinet cleared 150 MW floating solar plant on Rihand dam. It will be the biggest such plant in India and is expected to be commissioned by May 2020. ReNew got 100 MW while Shapoorji Pallonji got 50 MW at a tariff of INR 3.36/ unit. With increasing land acquisition problems for utility-scale solar, floating solar plants make a good business case for developers.

At about 300 GW, the potential of floating solar plants is huge in India, which can be achieved by utilizing just 10-15% of water bodies in states such as Kerala, Assam, Odisha, and West Bengal.

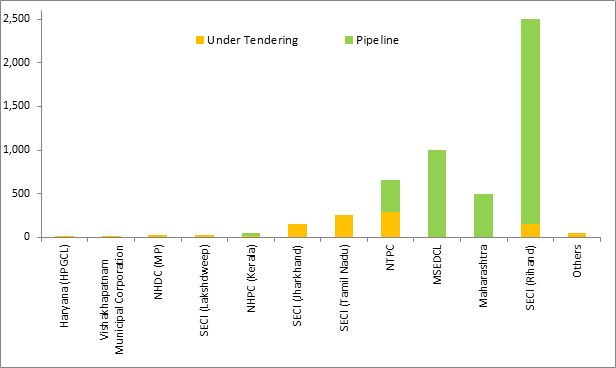

By 2020-21, the government of India has set a target to add 10 GW of floating solar capacity. As of July 31, 2019, about 2.72 MW of such solar plants are already commissioned while another 971 MW are under the tendering phase. Additionally, about 4,255 MW of new plants have been announced by various agencies where tenders are not yet released. Together, this will contribute to nearly 52% of the total target planned by the government. However, as per the current situation, achieving 10 GW target in the next two years is highly ambitious.

Figure 1: Status of floating solar projects in India (MW), as of July 31, 2019

Source: JMK research

Majority of these plants are planned in the states of Maharashtra, Uttar Pradesh, Jharkhand, Telangana, Tamil Nadu, and Andhra Pradesh. Active players participating in these tenders are ReNew, Shapoorji & Pallonji, S&W, Mahindra, Waaree and BHEL.

Despite being land neutral, the development cost of the floating systems including anchoring, installation, maintenance, and transmission is about 30-50% higher than the ground-based systems. However, the generation from these floating plants is higher as the panels’ efficiency is higher (about 6% to 7%) due to the cooling effects of water.

For successful tenders, the tariff range for floating plants is INR 3.29- 3.36 per unit. Whereas, for tenders with low ceiling tariffs (INR 3/ unit), like MSEDCL 1,000 MW in Maharashtra, they have failed to attract any bidders.

In price-sensitive markets like India, higher costs of floating solar plants will remain a big challenge. Other challenges such as rusting, corrosion, long term impact of moisture on modules, cables, non-availability of floats in India, etc. still need to be addressed to increase large scale adoption of floating solar power projects in India.