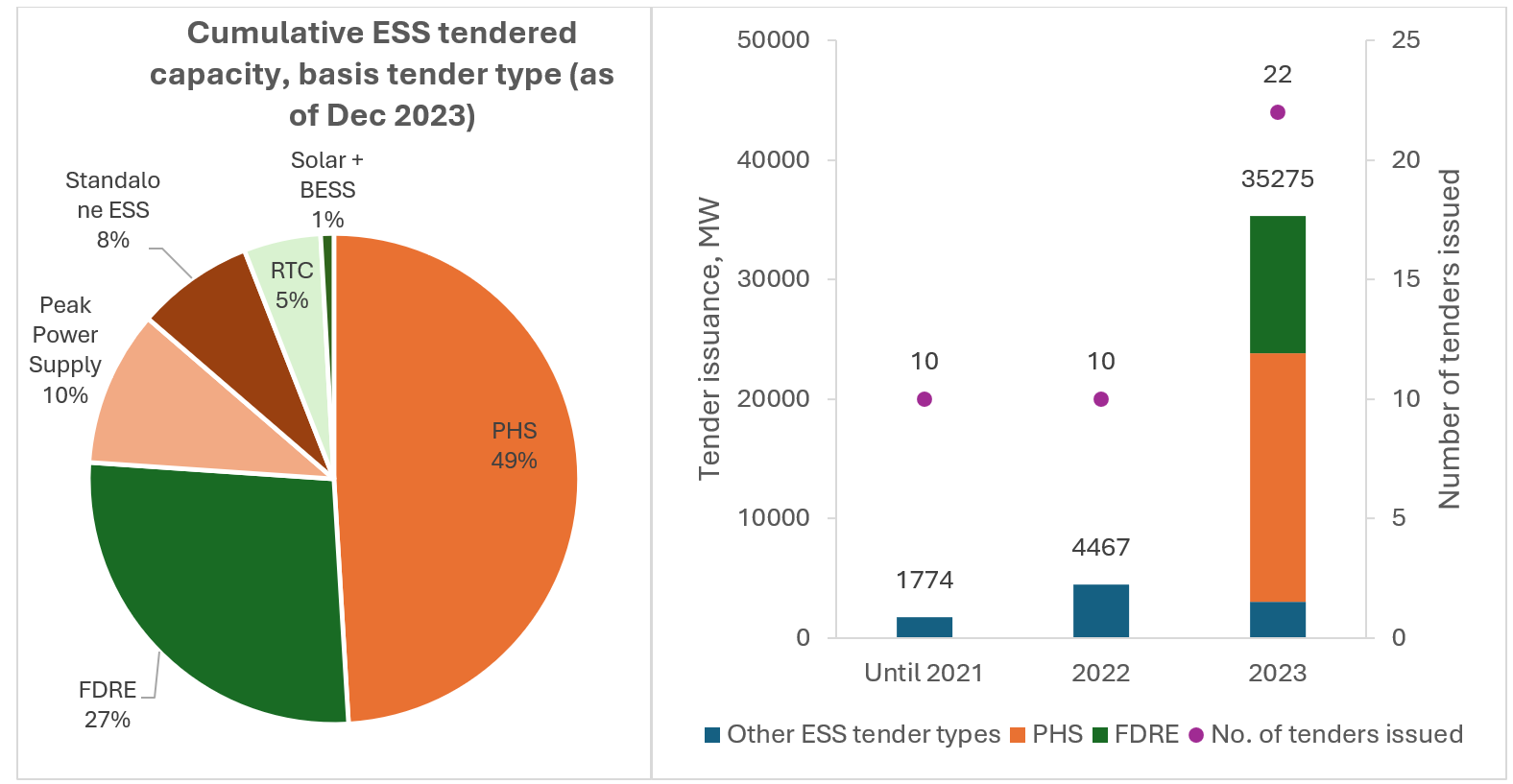

Pump Hydro Storage and FDRE tenders accounted for 91% of the entire ESS tender issuance in 2023

Akin to the rise of renewables, large-scale tendering is playing a crucial role in the growth of the Energy Storage Systems (ESS) market in India. Over the past few years, grid-scale ESS tendering in India has had unprecedented growth. Remarkably, tender issuance for grid-scale ESS in India (including pump hydro storage) has shot up by >35 GW in 2023 alone.

Over the years, grid-scale ESS tendering has had various iterations and tender types including solar + BESS, peak power supply, Round The Clock (RTC), standalone ESS. Until 2021, only 1,794 MW of grid-scale ESS capacity was awarded, excluding cancelled or dormant tenders. In 2023, two new entrants to ESS tender evolution have taken centre stage i.e. Pumped Hydro Storage (PHS) and firm and dispatchable Renewable Energy (FDRE). Together, they accounted for around 91% of the entire ESS tender issuance in 2023.

Figure 1: ESS tender issuance in India

Source: Tendering authorities, news articles, JMK Research

Note: The compilation excludes cancelled and dormant ESS tenders

Grid-scale PHS tender issuance capacity in 2023 was more than 20 GW, a meteoric rise compared to prior years, wherein no ESS tender was exclusively specified for PHS. Rewa Ultra Mega Solar Limited (RUMSL) issued the largest-ever ESS tender in June 2023 for 16.4 GW PHS capacity spread across 14 sites in Madhya Pradesh.

FDRE, the latest mutation of the ESS tender evolution, enables power procurement on a “demand-following” basis, creating a viable alternative to coal, hydro, and other dispatchable power-based technologies. Since its introduction in mid-2023, more than 90% of non-PHS storage tenders issued in India are FDRE.

The key differentiator of FDRE tenders from previous variations, such as RTC tenders, is the enhanced clarity for the project developers on the quantum, duration and schedule of the injected power requirement for the entire project tenure of 25 years. These characteristics will aid the developers in efficiently sizing the system and accurately modelling the future realised revenue, leading to correct tariff discovery.

In terms of ESS technology, in the near term, large grid-scale ESS will favour PHS, mainly due to its low levelized cost of energy (LCOE), especially for long-duration storage. However, with the likely decline in battery prices, BESS may overtake PHS as the most financially viable option to implement grid-scale ESS. In the long term, with green hydrogen-based ESS possibly attaining parity with PHS and BESS, green hydrogen may also become the dominant grid-scale ESS technology.

For India to attain the target as set by Central Electricity Authority (CEA) in its “Optimal generation mix report 2030” i.e. 41.7 GW/ 208 GWh of BESS and 18.9 GW of PHS, a concerted effort by all market stakeholders is imperative. Over the next decade, the widespread deployment of utility scale ESS will be crucial for sustainable addition of intermittent and variable renewable energy capacity to grid infrastructure.

To buy our comprehensive premium report on this topic, click here for more details.