Majority of equity investments in India’s rooftop solar segment are from foreign entities

Accessible financing is a prerequisite to drive growth in the rooftop commercial and industrial (C&I) solar market in India. Presently, the C&I segment accounts for almost 75% of the total rooftop solar installations in India with annual additional installations of 1.3 gigawatts (GW) to 1.8GW in the last few years. In light of this, it becomes imperative to analyze how these players have been able to finance these projects and what trends can be extracted from our analysis.

There are four ways to access funds for rooftop solar installations: equity investments, debt capital, mergers & acquisitions, and via loans or concessional credit lines. In this series of four blogs, we will analyze each of the different routes through which investments have been raised by players, starting with equity investments in this blog.

Equity Investments

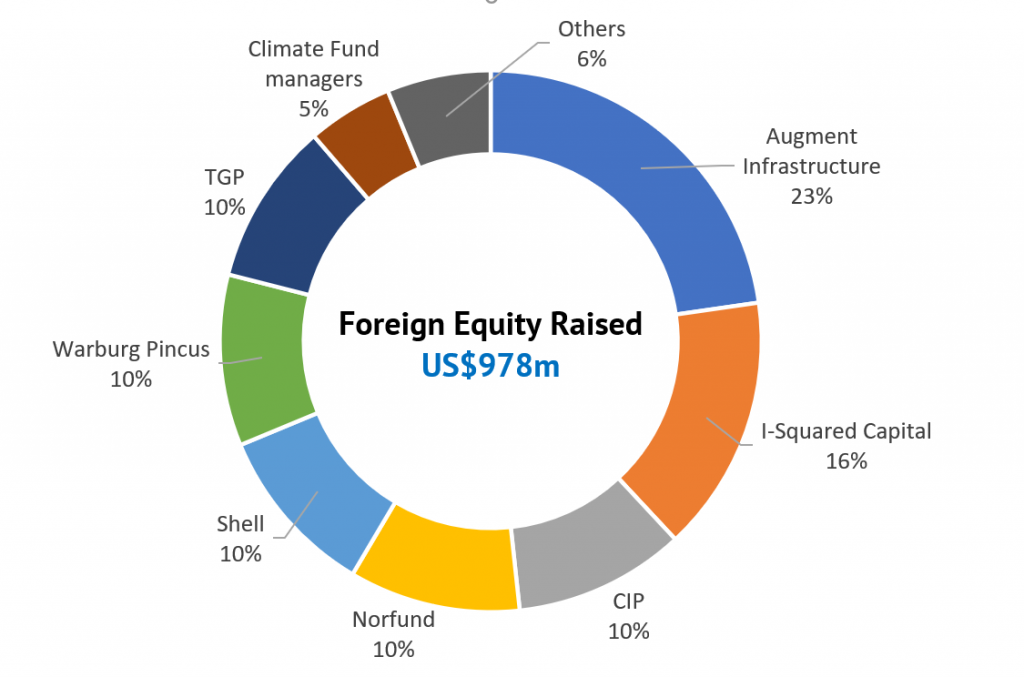

From Jan 2015 till August 2021, project developers active in rooftop solar space have raised over US$2bn investments. 48% (US$985mn) of these investments came from equity funding. Equity investments are vital for the rooftop solar segment to achieve the scale needed to establish this technology as a bankable asset. An interesting trend to note here is that almost all equity investments come from foreign entities (99%) which are looking to enter the Indian market, due to its high growth potential, longer PPA durations, and the ability for foreign entities to own 100% of the asset. The largest share of 23% is accounted for by Augment Infrastructure Investments, a US investment firm, which acquired Warburg Pincus’ minority stake in CleanMax in August 2021 for US$ 100 mn.

Fig 1: Foreign Equity Investments Raised

Source: IEEFA, JMK Research

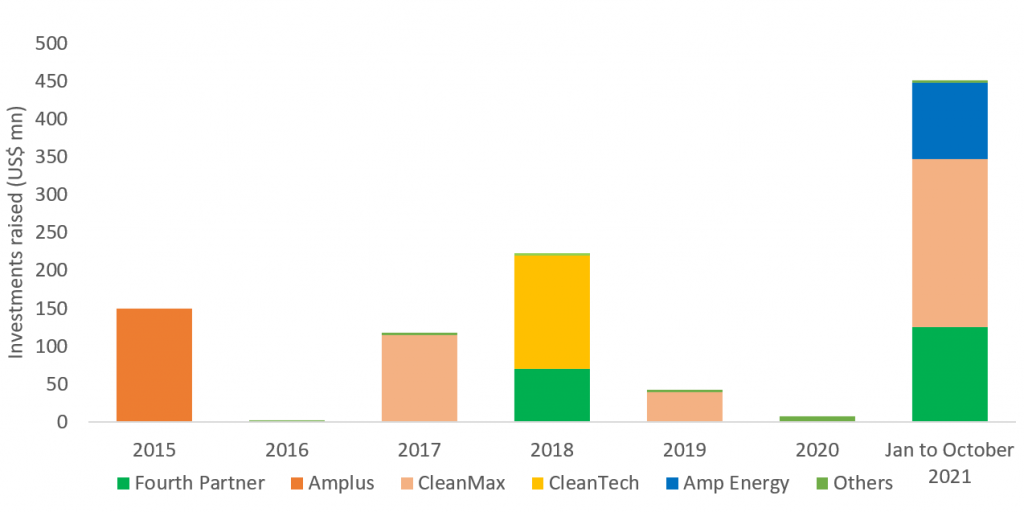

As depicted in figure 3, equity investments in the segment are concentrated within the established players in the market such as CleanMax (38%), Fourth Partner (20%), Amplus (15%), CleanTech (15%) and Amp Energy (10%). Over 45% of the total equity investments were raised in 2021 itself. The key reasons behind equity investments being concentrated within the abovementioned players are these players’ substantial experience in the Indian solar market, sizeable portfolios, bankable track records, and the fact that the portfolios of these players are spread across different states in India, which reduces risks for investors.

Fig 3: Equity Investments Raised (2015-Present)

Source: IEEFA, JMK Research

While equity funds have played a pivotal in scaling rooftop solar in the C&I segment, these funds are not accessible to all interested players. For these players, there are other routes to raise funds to finance the project, which will be covered in subsequent blogs.

Click below to access our report, co-authored with IEEFA, for in-depth analysis on the financing trends in the C&I Rooftop solar space