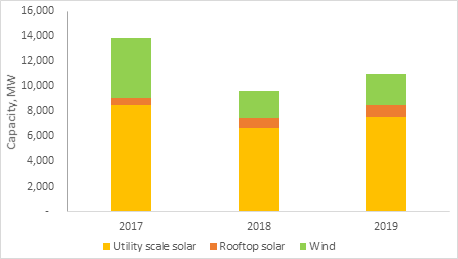

India installs 7.5 GW of utility-scale solar and 2.4 GW of wind in CY2019

India’s renewable capacity installations reached 86 GW as of December 31, 2019. Wind is the major contributor with 44% share in total renewable mix, followed by solar with 39% share. In last one year, the share of solar rose by 5 percentage points to about 39%.

In CY2019, about 7.5 GW of new utility-scale solar capacity was added, which is about 14% increase over the previous year. Another 1 GW was added in rooftop solar installations. Karnataka led the market with about 2 GW of new solar capacity additions followed by Rajasthan (1.7 GW), Tamil Nadu (1.5 GW), Gujarat (936 MW), Andhra Pradesh (917 MW) and Madhya Pradesh (651 MW). NLC, ReNew, Azure, and Acme were the leading project developers to add maximum solar capacity in 2019.

Total solar capacity added fell short of CY2019 projections by JMK Research & Analytics. We estimated about 8.5 GW of new solar capacity based on the project allotment schedule under various state and central tenders in 2017-18. A lot of projects which got delayed are now likely to get commissioned in the first half of 2020. These delays are primarily due to land acquisition issues, execution delays, delay by DISCOMs (secondary power off-taker) in submitting approvals to SERCs for tariff adoption, policy uncertainty because of regressive net metering guidelines and withdrawal of open access benefits, retendering etc.

On the wind side, In CY2019, about 2.4 GW of new wind capacity is added, which is a 10% increase over CY2018. Gujarat led the installations with commissioning of 1.4 GW of new wind projects followed by Tamil Nadu (650 MW) and Maharashtra (212 MW). Most of the wind projects allocated in 2018 and scheduled to commission in 2019 got delayed and are now likely to be commissioned in 2020. This delay in wind projects is primarily attributed to various land availability issues and lack of grid transmission availability. SembCorp, Mytrah, ReNew and Greenko were the leading players which added maximum wind capacity in 2019.

Figure 1: Year-wise RE installation trends in India

Source: MNRE, JMK Research