Impact of EV transition on domestic auto ancillary market

Regarded as the world’s sourcing hub for automobile components, the Indian auto component industry has witnessed strong revenue growth of about 13% CAGR from 2013 to 2019 to reach USD57 billion[1]. Out of the total FY2019 revenue of USD57 billion, approx. 65% is contributed by sales to domestic Original Equipment Manufacturers (OEMs). While the remaining 35% comes from export and aftermarket/ replacement segment.

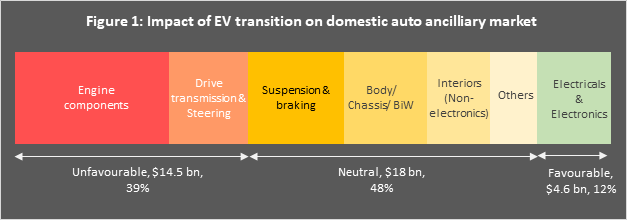

With the automotive sector transitioning towards electric mobility, the domestic auto ancillary market is also going to witness significant changes. The electrical and electronic components market such as motors, batteries, and power electronics would still see a gradual yet robust uptake. While the impact is expected to be neutral for other components such as suspension, braking, body chassis, BiW, interiors (non-electronics), etc.

Adverse impact of EV transition will be witnessed by the engine components (piston, engine valves, fuel injection systems, etc.) and drive transmission parts. However, there is a vast untapped potential of the alternate new segment of EV batteries and powertrain technologies which would emerge. This would present an enormous growth opportunity for market players in the near future.

* FY2019 market size for auto ancillary supply to domestic OEMs – USD37 Billion

Source: ACMA website, JMK Research

The Indian automotive market has already started exploring new business models to stay afloat and adapt to the changing market environment. The giants in the auto parts business such as Bharat Forge, Bosch, TVS, JMT Auto who have a wide array of auto component portfolios have already advanced into the electric mobility segment. Backed up by constant R&D effort, these players have started offering quality solutions in the design and development of motor, inverter, and battery management systems.

[1] Source: The Automotive Components Manufacturing Association (ACMA) website