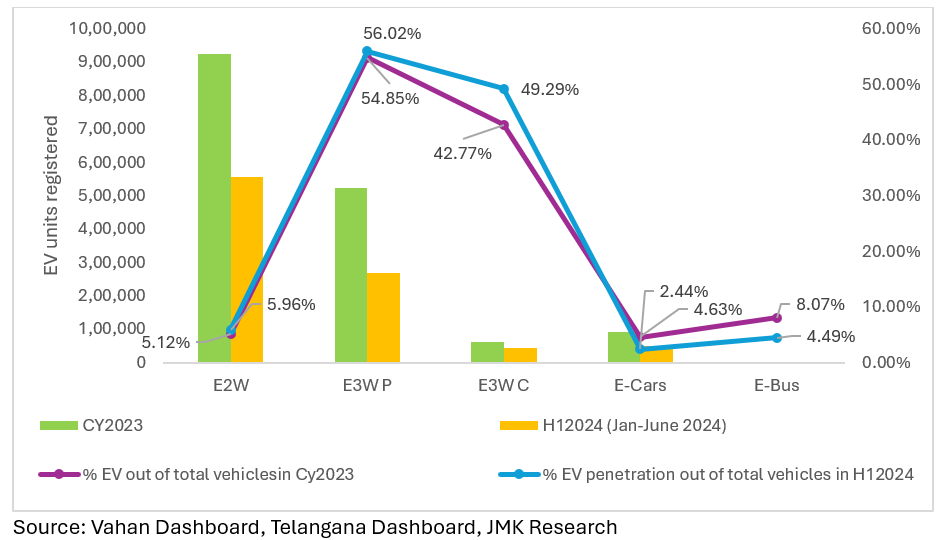

EV Sales in India increased by 21% in H1 2024

Electric vehicle (EV) sales in India reached an impressive 9,27,097 units in H12024 (Jan-Jun-24), with the E2W and E3W passenger segments leading the charge, accounting for 89.13% of the total sales. Sales have increased by 20.73% in H12024 compared to H12023 EV sales.

- E2W sales reached 5,56,091 units in H1 2024, about 58% of the total E2W sales in CY2023.

- In H12024, sales in the E3W passenger segment reached 2.70 lakh units, accounting for nearly 51% of the total E3W passenger sales in 2023. This indicates that sales have remained stagnant and are expected to reach figures similar to last year’s by the end of 2024.

- E3W Cargo sales were 45,265 units in H1 2024, 72% of the sales in CY2023. This indicates that sales this year are projected to significantly exceed those of last year. The electrification rate in this category has hit almost 49.2%, driven by increasing demand from the logistics and last-mile delivery segments.

- E-car sales reached 49,694 units in H12024, almost half of the sales in CY2023. Sales are expected to be slightly higher than last year, with a boost anticipated from the upcoming festival season.

- E-bus sales have reached 1,924 units in H1 2024, amounting to nearly 70% of the total sales in 2023. Sales are projected to surpass last year’s figures, driven by new tenders and the central and various state government’s focus on public transport electrification.

Fig 1: EV sales trend in India in H12024 Vs. CY2023

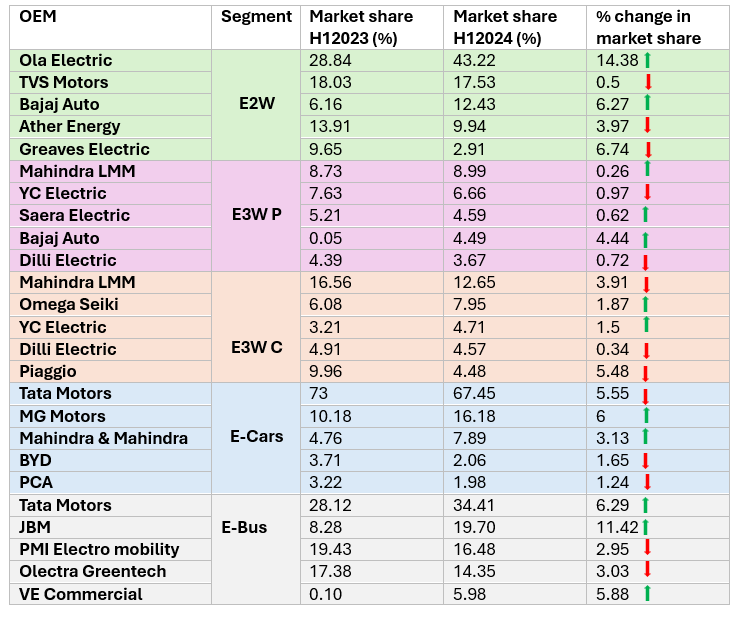

In terms of leading players’ market share, following trends are seen:

- In the E2W segment, Ola Electric remains the market leader, with over 2.40 lakh units registered in H12024, capturing a 43% market share. The top five players collectively account for 86% of the total E2W market.

- The E3W Passenger segment is a highly fragmented market with over 400 players. Notably, Bajaj Auto entered the top 5 in H12024, with a 4.44% increase in market share.

- In the E3W Cargo segment, Mahindra LMM has seen a ~4% decline in market share compared to last year; however, it remains the market leader in H1 2024.

- Despite a 6% decline in market share in the E-Car segment, Tata Motors remains the market leader in H12024. Meanwhile, MG Motors and Mahindra market share increased a bit which is mainly driven by launch of new models this year.

- In the E-Bus category, Tata Motors, JBM, and VE Commercial have all seen a significant increase in market share in H12024, with Tata Motors continuing to lead the category as it did last year.

Table 1: Comparison of EV OEM Market Shares: H12023 Vs. H12024

Source: Vahan Dashboard, Telangana Dashboard, JMK Research

The above figures clearly indicate that sales in CY2024 are likely to be better than sales in CY2023 across all segments. Furthermore, with FAME III on the horizon, the anticipated incentives are set to further drive EV sales and boost market growth.