E-Buses: India Market Analysis

Executive Summary

There is a tremendous underlying opportunity for an effective delivery of road transport service in India. The advent of electric buses (e-buses) will pave the way for future of efficient mass public transport system. Apart from being cleaner and greener, the major advantage of an e-bus is its extremely low operational and maintenance (O&M) expenditure per unit km. The Total Cost of Ownership (TCO) of e-buses is 10-20% lesser than that of diesel buses.

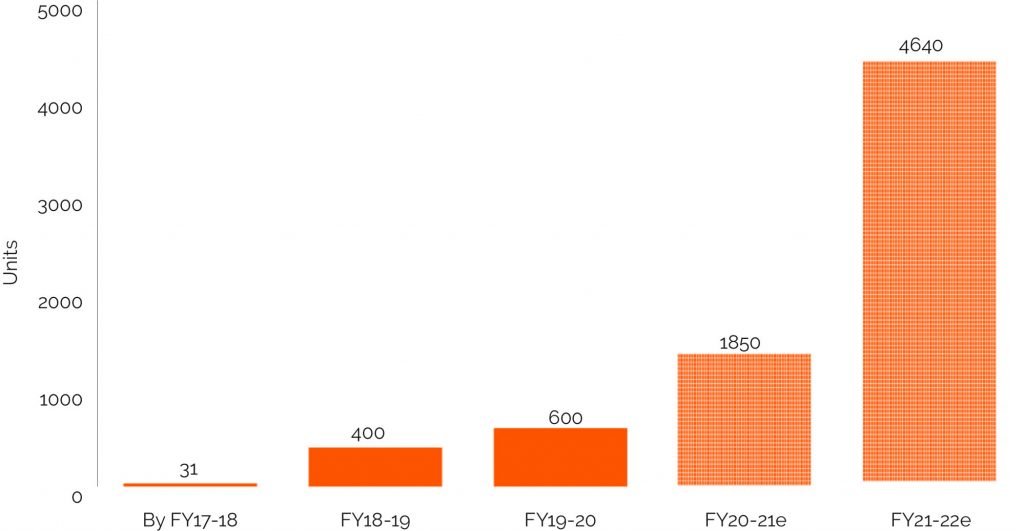

In September 2017, the first commercial e-bus operations began in India in Himachal Pradesh. Since then, the e-bus market has evolved substantially. By March 2020, about 1,031 e-buses were sold across different states and transport undertakings. As per JMK Research estimates, additional 1850 buses are likely to be sold in FY2021 and around 4640 units in FY2022.

E-Bus sales in India

Source: FY17-18 till FY19-20 numbers are taken from SMEV, projections for FY20-21 and FY21-22 by JMK Research

The e-bus market growth is fuelled by more than US$1 Bn worth of investment deals forged in the past few years with investors of varied business backgrounds. To keep up with the pace of e-bus induction and deployment onto the public roads, the charging systems and allied-infrastructure must also be enhanced and/or developed systematically to overcome local-specific challenges. Henceforth, this report shall briefly touch upon the significant developments in the Indian e-bus market, policies, tender analysis, charging infrastructure and so on.

Contents

- Executive Summary

- Market Overview

- TCO Analysis of Diesel v/s Electric buses

- Modes of E-bus procurement

- Outright purchase model

- Gross Cost Contract model

- Policies

- Central Policies

- State policies

- Tender analysis

- Market Size

- Investments

- Charging Infrastructure

- Key Players

- Conclusion

To download the full report